Future Value Compound Interest Formula: A Clear Guide to Growing Money

The future value compound interest formula is one of the most useful tools in personal finance. It tells you how much a sum of money will be worth after earning interest over time. The future value interest factor is the multiplier that scales your initial investment based on rate and time. Whether you are calculating the future value of a lump sum or working out the future value of a single amount saved today, the same core math applies. The future value of perpetuity is a special case that shows what an infinite stream of payments is worth right now.

Understanding these concepts gives you real power over financial planning. Let’s break each one down clearly so you can use them with confidence.

How the Future Value Compound Interest Formula Works

Breaking Down the Future Value Interest Factor

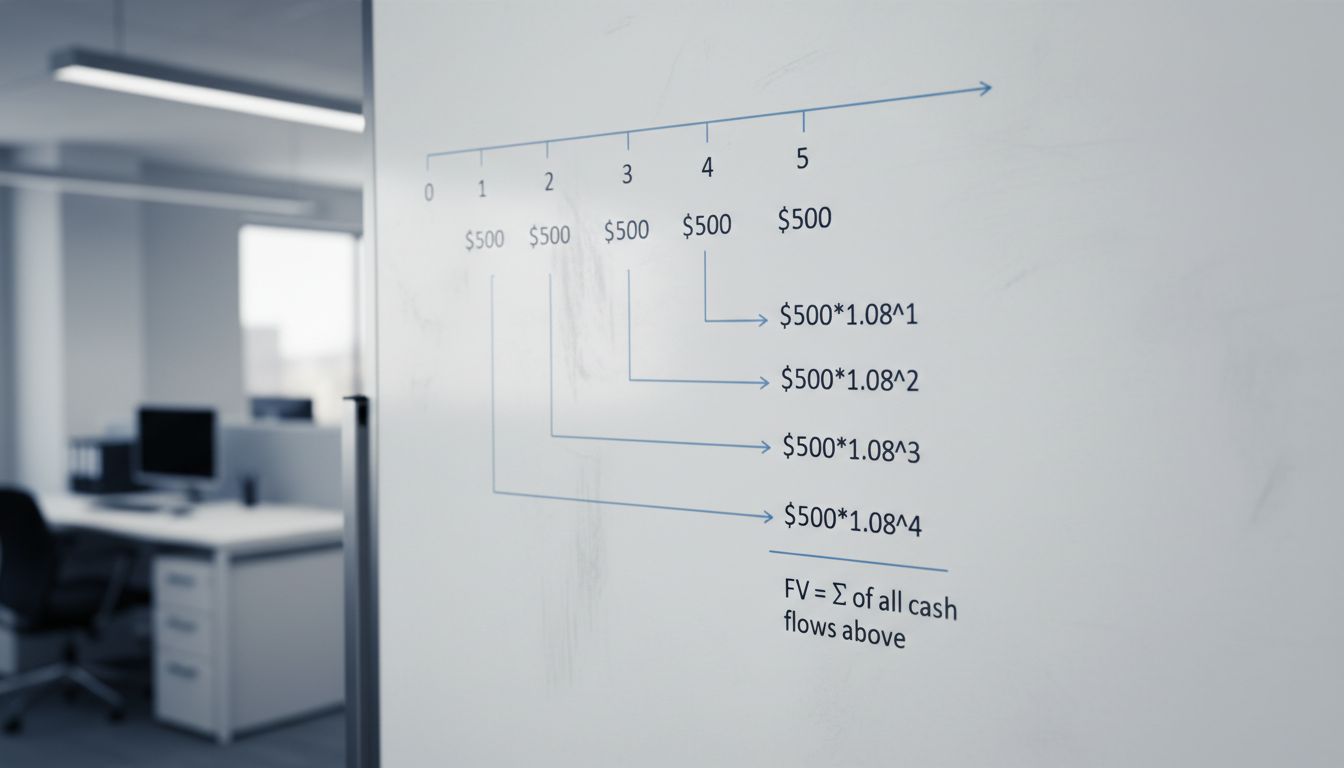

The future value compound interest formula is: FV = PV x (1 + r)^n. In this equation, PV is the present value (what you start with), r is the interest rate per period, and n is the number of periods. The future value interest factor — often abbreviated FVIF — is the (1 + r)^n part. It tells you how much each dollar grows over time at a given rate.

For example, if you invest $1,000 at 5% annual interest for 10 years, the future value interest factor is (1.05)^10, which equals about 1.629. Multiply that by $1,000 and you get $1,629. That is compound growth in action. The future value compound interest formula makes this calculation straightforward.

Compounding frequency matters. If interest compounds monthly rather than annually, you adjust the formula: divide the annual rate by 12 and multiply the number of years by 12. More frequent compounding means faster growth. The future value of a lump sum grows faster with monthly compounding than with annual compounding at the same nominal rate.

Future Value of a Lump Sum vs. Future Value of a Single Amount

When These Terms Mean the Same Thing — and When They Don’t

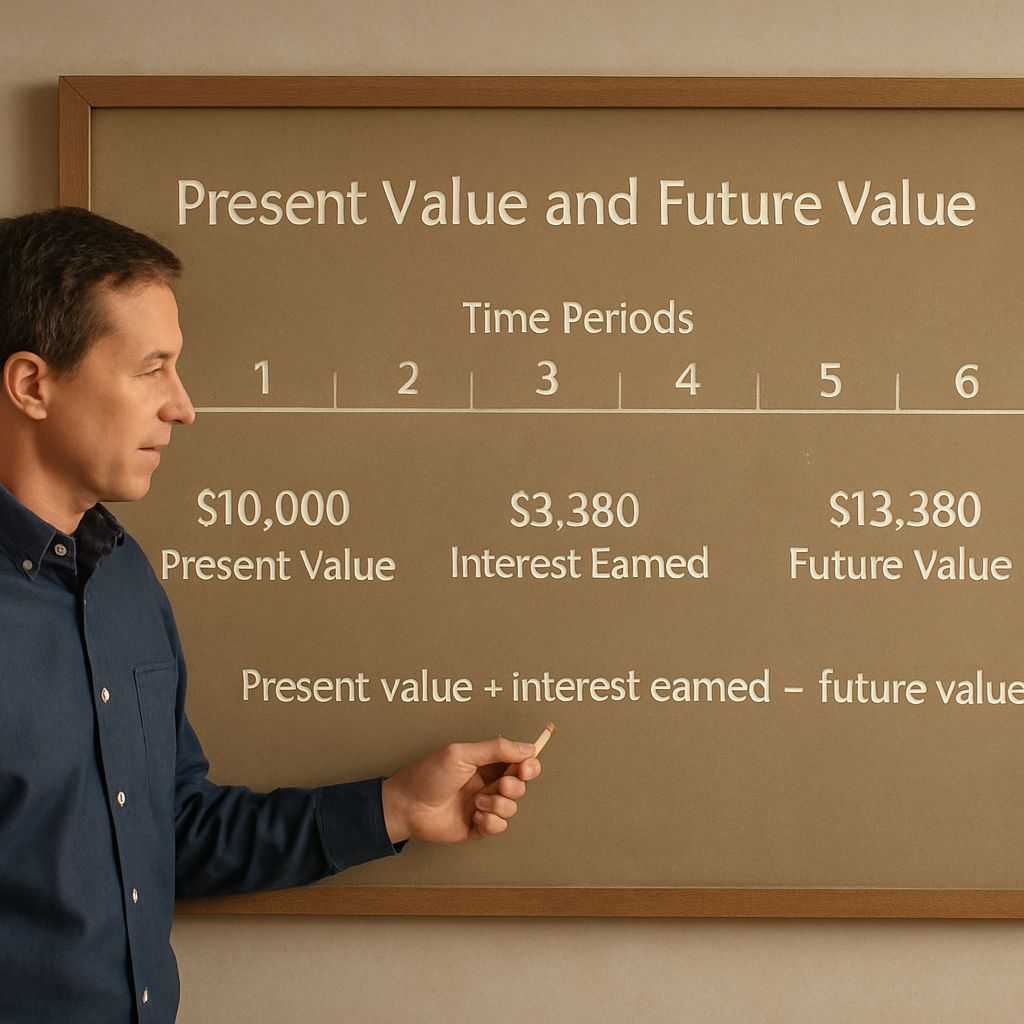

The future value of a lump sum and the future value of a single amount refer to the same concept: you invest a one-time sum now and let it grow. The terminology differs by textbook and instructor, but the math is identical. Both use the future value compound interest formula: FV = PV x (1 + r)^n.

Where confusion sometimes arises is with annuities. An annuity involves regular payments, not a single deposit. The future value of a single amount is distinct from the future value of an annuity, which requires a different formula. If you are calculating a single deposit invested over time, you want the lump sum version.

Practical uses for the future value of a lump sum include retirement planning, college savings, and investment projections. If you know your present savings, your expected return, and your time horizon, this formula gives you a concrete target. The future value of a single amount shows you where you will end up if you stay the course.

The Future Value of Perpetuity Explained

The future value of perpetuity is a concept that applies when a cash flow stream has no end date. A perpetuity pays a fixed amount forever — think of certain bonds or endowments. The present value of a perpetuity is PV = C / r, where C is the regular payment and r is the discount rate.

Technically, the future value of perpetuity at any finite future point is still infinite, since the payments keep coming. In practice, analysts use perpetuity formulas to value long-term income streams where the end date is uncertain or very far off.

Perpetuity math also connects back to the future value interest factor. If you discount a perpetuity back to today using a given rate, you are applying the same compounding logic in reverse. The future value compound interest formula and perpetuity valuation are two sides of the same coin.

Applying These Formulas in Real Financial Decisions

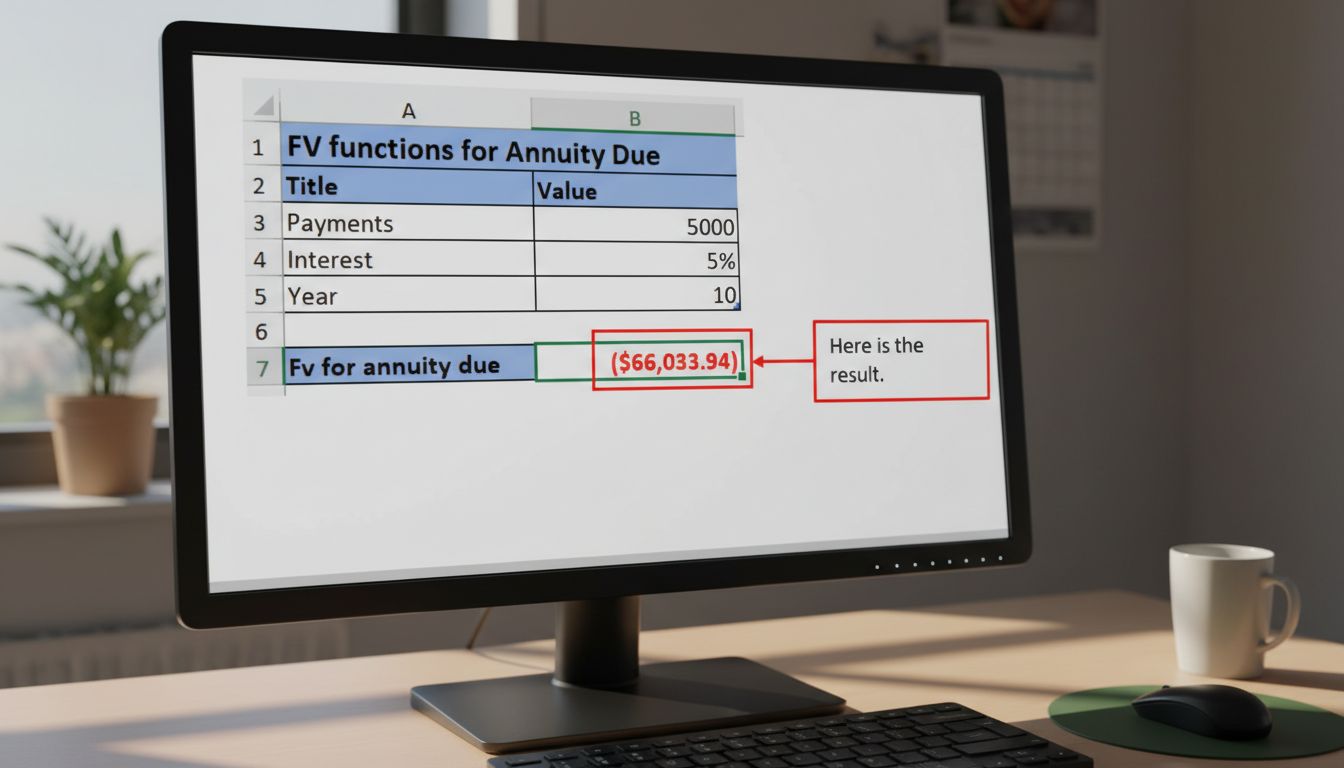

The future value of a lump sum formula is the first thing to use when evaluating a savings plan. Enter your starting balance, expected return, and years to goal. The result tells you whether you are on track or need to adjust. Many online calculators do this automatically, but knowing the formula lets you check the math.

For longer-term planning, the future value interest factor tables are useful reference tools. These pre-calculated tables show the FVIF for various combinations of rate and period. You simply look up the factor and multiply by your starting amount. The future value of a single amount is then easy to compute without a calculator.

Knowing the future value of perpetuity helps when comparing investment vehicles that promise indefinite income. A financial product paying $500 per year indefinitely at a 4% discount rate has a present value of $12,500. That benchmark helps you decide whether the price being asked is fair.

Bottom line: the future value compound interest formula, the future value interest factor, and the future value of a lump sum are foundational tools for any financial plan. Master these and you can evaluate nearly any savings or investment scenario with confidence.