Future Value Table: How to Read and Use It for Financial Planning

A future value table is one of the most practical tools in personal and business finance. It lets you look up a pre-calculated growth factor based on interest rate and time period, then apply it to any starting amount. The future value of 1 table specifically shows you how a single dollar grows at various rates over time — which is the building block for all other future value calculations. The broader category of present and future value tables includes tables for both single amounts and annuities. When you need to look up multiple rates or periods quickly, future value tables eliminate repetitive calculation. The future value of a dollar table is the most common version used in accounting courses and financial planning contexts.

This guide explains how to read these tables, when to use them, and what each table type tells you.

How to Read a Future Value Table

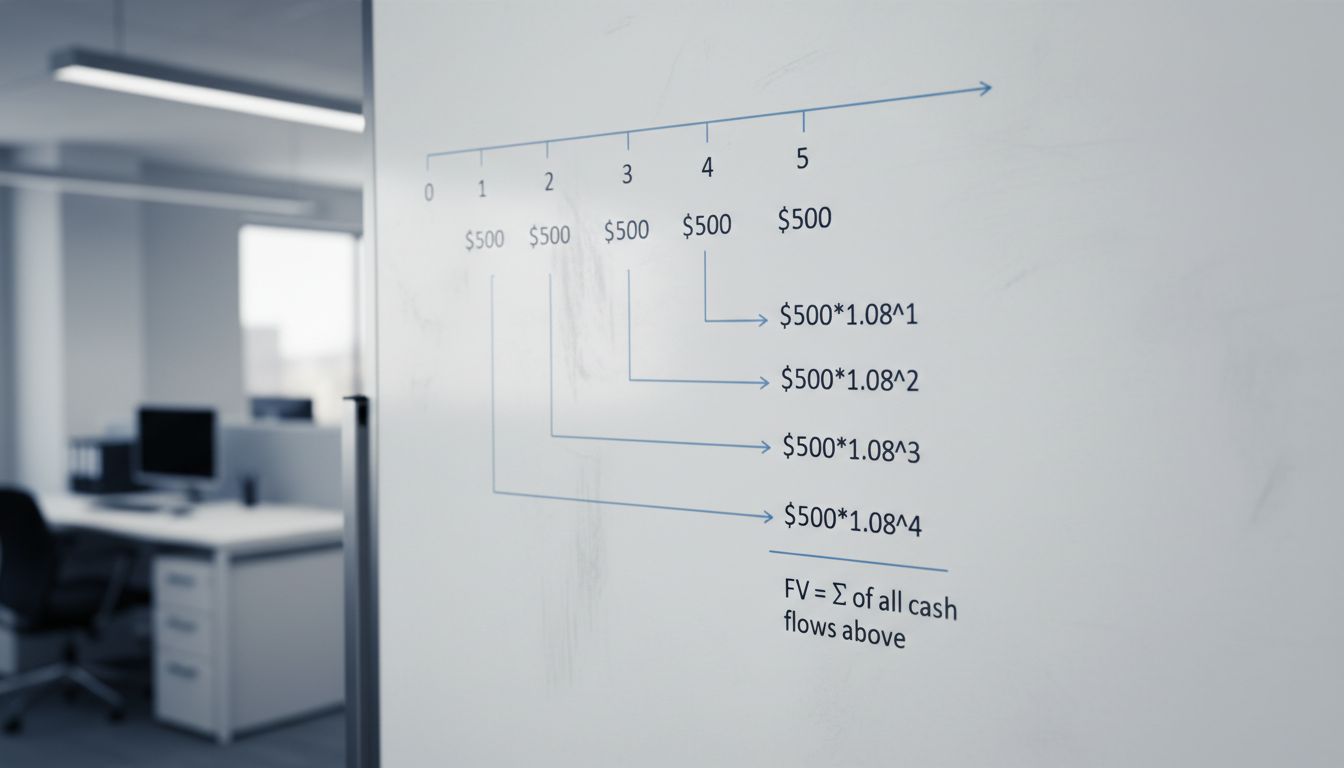

The future value table is organized with interest rates across the top row and number of periods down the left column. Each cell contains a factor — a multiplier you apply to your present value to find the future value. The formula it represents is: FV = PV × (1 + r)^n. The table pre-calculates the (1 + r)^n part, so you just multiply.

Example: You invest $5,000 at 6% annual interest for 10 years. Find 6% across the top of the future value of a dollar table, find 10 periods down the left side, read the factor (approximately 1.791). Multiply: $5,000 × 1.791 = $8,955. That is your approximate future value. The table saves you from computing (1.06)^10 by hand.

Most future value tables cover interest rates from 1% to 20% and periods from 1 to 40. If your rate or period falls outside those ranges, you will need a formula or calculator instead. For most standard financial planning scenarios — retirement accounts, savings goals, loan comparisons — the table covers everything you need.

Future Value of 1 Table vs. Annuity Tables

The future value of 1 table covers a single lump-sum amount — one payment made today, growing over time. If you deposit $10,000 now and want to know what it will be worth in 20 years at 5%, you use the future value of 1 table.

Annuity tables cover a series of equal payments made at regular intervals. The present and future value tables in most textbooks include both single-amount tables and annuity tables side by side. If you are contributing $300 per month to a retirement account, you use the future value of annuity table, not the future value of 1 table. Mixing these up is the most common error when students and non-accountants use these tables.

The future value of a dollar table and the present value of a dollar table are mirror images. The present value table tells you what a future dollar is worth today at a given discount rate. The future value table tells you what today’s dollar will be worth at a future date at a given growth rate. Both use the same factor system — just applied in opposite directions.

Practical Uses of Future Value Tables

Present and future value tables appear in accounting courses, CPA exam preparation, MBA finance classes, and real-world financial planning. Accountants use them to value lease obligations, bonds, and pension liabilities. Financial planners use them to project retirement savings, education fund growth, and insurance policy values.

For individuals, the future value table is most useful when comparing savings scenarios. Want to know if doubling your monthly contribution makes a bigger difference than increasing your interest rate by 1%? Run both numbers through the table side by side and compare. The visual comparison reveals the compounding effect in concrete dollar terms rather than abstract percentages.

Next steps: Find a future value of 1 table online or in any introductory finance textbook. Look up the factor for your current savings interest rate and your time horizon. Multiply that factor by your current savings balance to see your projected value. Then try a 1% higher rate to see the compounding difference. This single exercise usually changes how seriously people take even small increases in their savings rate or investment returns.