Future Value of Ordinary Annuity Calculator: How to Use It and Why It Matters

A future value of ordinary annuity calculator takes three inputs — payment amount, interest rate, and number of periods — and tells you what your series of regular payments will be worth at a future date. The formula for future value of annuity is the math behind that calculation. Using a future value of an ordinary annuity calculator saves time when working with retirement accounts, savings plans, or any structured payment schedule. If payments occur at the beginning of each period rather than the end, you need a future value of annuity due calculator instead. Both tools use the same core logic, but the timing difference changes the result. A future value ordinary annuity calculator is the right choice for most standard financial planning scenarios.

This article explains the formula, walks through the difference between ordinary and due annuities, and shows you how to use these tools effectively.

The Formula for Future Value of Annuity: Breaking It Down

The formula for future value of annuity for an ordinary annuity is:

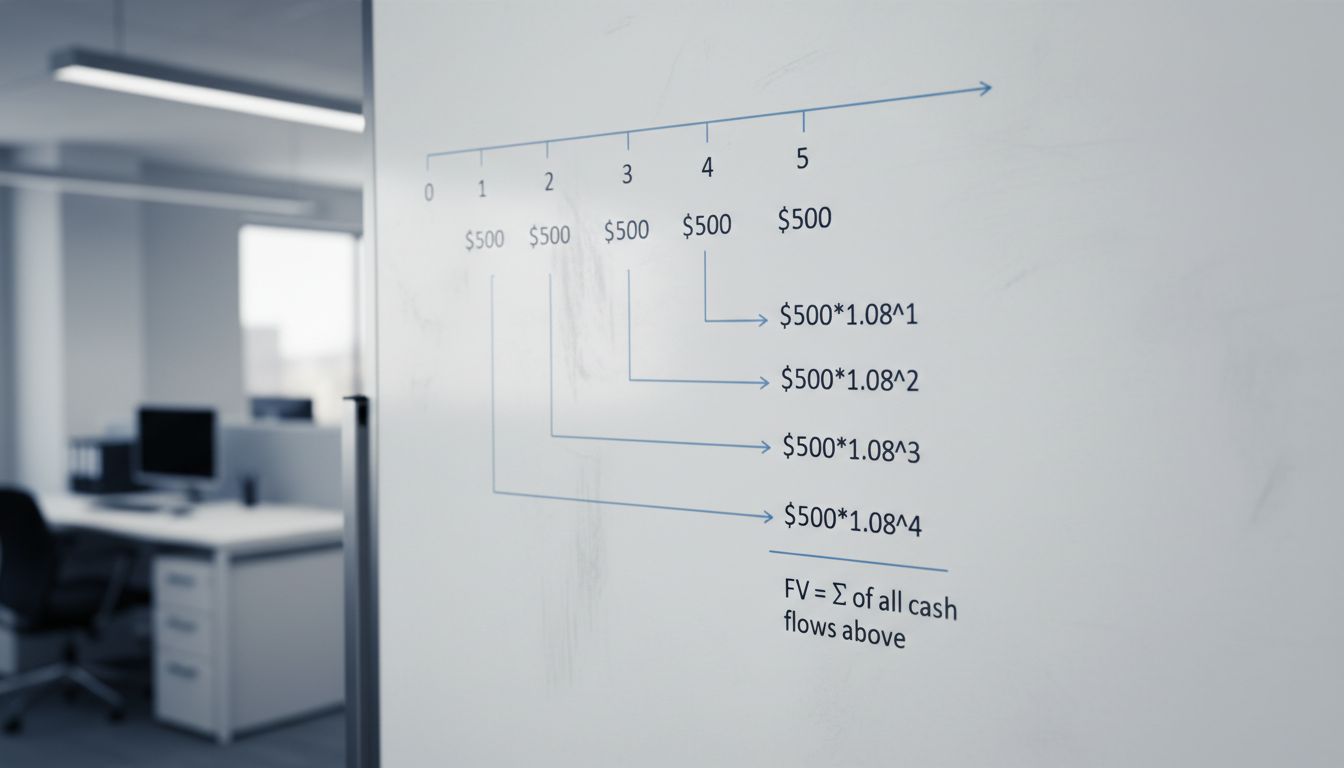

FV = PMT × [(1 + r)^n – 1] / r

Where: PMT = payment amount per period, r = interest rate per period, n = total number of periods.

Example: You deposit $300 per month into a savings account earning 5% annual interest (0.4167% per month) for 10 years (120 months). The future value ordinary annuity calculator applies the formula: FV = 300 × [(1 + 0.004167)^120 – 1] / 0.004167. The result is approximately $46,550 — your 120 deposits of $300 grew to nearly $46,600 through compounding.

The future value of ordinary annuity calculator does this math instantly. But knowing the formula helps you understand what the calculator is actually doing and how changing any input affects the result.

Ordinary Annuity vs. Annuity Due: Which Calculator to Use

The future value of an ordinary annuity calculator assumes payments at the end of each period. This is the standard setup for most savings plans, mortgage payments, and investment contributions. When you contribute to your 401(k) at the end of each month, that is an ordinary annuity.

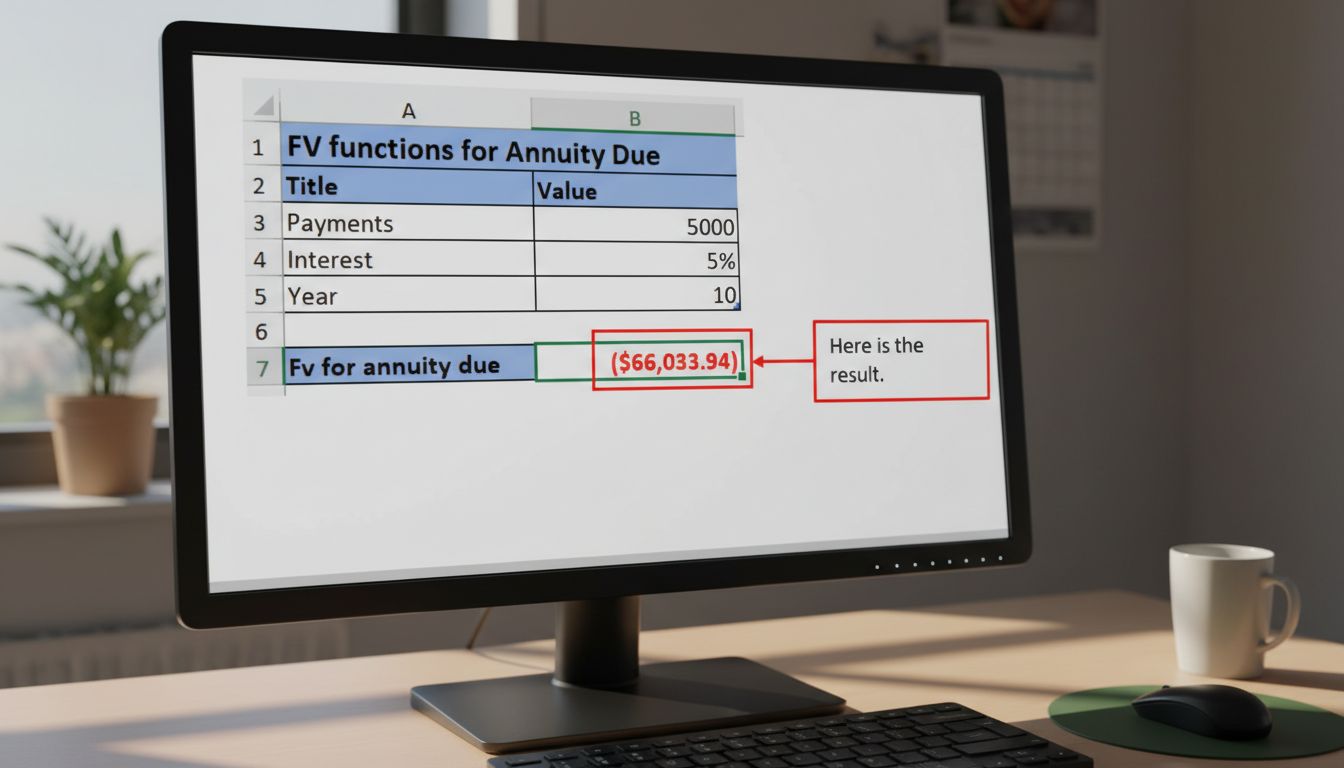

The future value of annuity due calculator assumes payments at the beginning of each period. Lease payments, rent, and insurance premiums are often structured this way. Because each payment earns one additional period of interest, the annuity due always produces a higher future value than the ordinary annuity with identical inputs.

The adjustment is simple: multiply the ordinary annuity result by (1 + r). If your ordinary annuity future value is $46,550 at 0.4167% per period, the annuity due future value is approximately $46,550 × 1.004167 = $46,744. A future value of annuity due calculator handles this automatically — you just need to select the correct payment timing before running the calculation.

How to Use a Future Value Ordinary Annuity Calculator Effectively

A future value ordinary annuity calculator works best when you treat it as a planning tool rather than just a lookup device. Run multiple scenarios by changing one variable at a time. Start with your expected payment amount, then test different interest rates to see how much rate matters. Then extend or shorten the time period to see how duration affects outcomes.

Key inputs to double-check before calculating: make sure your interest rate and period count match. If you are contributing monthly, use a monthly rate (annual rate ÷ 12) and count months, not years. A common error is entering an annual rate with a monthly period count, which overstates the result significantly.

The future value of an ordinary annuity calculator also works in reverse. Many tools include a “solve for payment” function. If you know you want $500,000 in 25 years and you expect a 6% annual return, the calculator tells you what monthly contribution gets you there. This reverse calculation is particularly useful for retirement planning and education savings.

Bottom line: The future value of ordinary annuity calculator is one of the most practical financial tools available. Know the formula, understand whether you need the ordinary or annuity due version, and run multiple scenarios before making long-term savings decisions.